Interest rates have risen dramatically in the last year. By some measures, interest rates increased faster in 2022 than in any of the previous forty years. As a result, yields on short-term CDs, bonds, and other income vehicles have become attractive. At the same time, eye-catching offers on income annuities have also been popping up. In this article we will examine the relationship between short-term interest rates, longer term interest rates, and the payout rates on income annuities.

What’s next for interest rates?

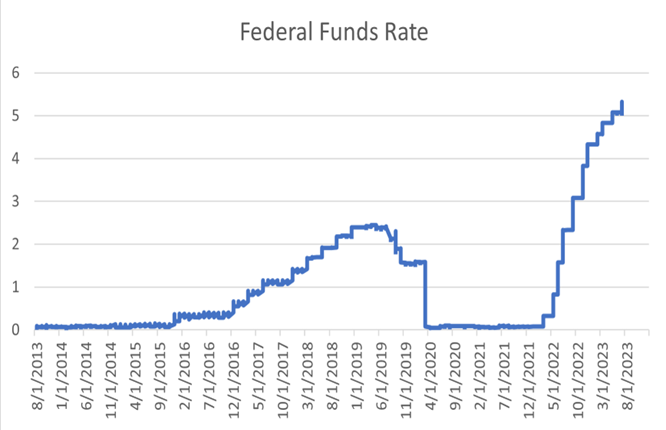

The Fed raised the federal funds rate by a quarter of a percent at their July meeting, following a string of ten consecutive rate increases, from near-zero to over five percent. That’s an increase of over 6,000%, the steepest spate of rate hikes in forty years. The sharp rise in interest rates can be tied to the US Federal Reserve’s efforts to fight inflation, which hit forty year-year highs last year.

The sharp increases in short-term rates appear to have cooled off the super-hot inflation. Now many expect the Fed to pause its rate hikes and then, starting in 2024, to begin cutting the fed-funds rate. This consensus can be seen in the relatively low yields on longer-term bonds. In fact, longer-term interest rates are actually lower than short-term rates, hence the “inverted” shape of the treasury bond yield curve.

What about bonds?

After years of low yields followed by a brutal drop in prices during 2022, returns in the fixed income markets appear poised to rebound. The Fed appears to be serious about fighting inflation, even at the expense of growth. If the Fed sticks to its tight policy stance, longer-term yields should continue to fall. This will be good for bonds. It’s likely to be a bumpy ride due to the cross currents created by global central banks, a volatile global economy, and political uncertainty. However, starting yields are the highest in years, and so a portfolio of high-quality bonds can yield attractive returns without excessively high risk.

FAQS

We’re happy to answer any questions you have about our firm and our processes. Here are answers to some of the questions we receive most frequently.

How do interest rates affect annuity payouts?

Annuities are income vehicles, so it’s natural to consider current interest rates and the outlook for future rates. But too often the relationship between some annuities and interest rates is misunderstood, and that often leads to less-than-optimum decisions.

There are many types of annuities, but let’s focus on two types of annuities that provide safe, guaranteed income: Single premium immediate annuities (SPIAs) and deferred income annuities (DIAs). SPIAs pay a fixed amount of monthly income starting immediately, and the income is guaranteed to last for as long as you live. DIAs provide fixed monthly income for as long as you live, beginning at a time you select that is two years or more in the future.

With straightforward income vehicles like these, interest rates are not the primary factor when deciding how much income to guarantee. The primary factor is your life expectancy -that is, how long the insurer estimates it is likely to have to pay income to you. Interest rates are still an important consideration, but long-term rates are much more important than short term rates. Annuity providers typically buy government bonds to generate returns. High interest rates push these returns up, so a rise in interest rates should push annuity rates up as a result. However, longer-term interest rates have not risen much, and are actually forecast to decrease.

ACCREDITATIONS & AWARDS

We’re proud to have been honored by some of the organizations in our industry.

Pitfalls of buying annuity contracts in this market

The higher short-term interest rates have allowed annuity companies to offer attractive initial payout rates, however these are just temporary. Annuity contracts are very long-term investments, and so short-term rates shouldn’t be a driver of your decision to buy an annuity.

Annuity products generate a lot of revenue for advisors and companies who sell them, so you really must be on your guard for hyped claims of their benefits. The reality is that annuities are complex vehicles. One can be quite different than another. Once you purchase an annuity, you may be stuck with it for many years. And because they are so complex, annuity contracts can be extremely hard to evaluate. This makes it easy to make a mistake when choosing an annuity.

At Blankinship & Foster, we help our clients with far more than investment management. We provide proactive, personalized advice on all aspects of their finances. Please contact us to learn more about how we can help you.

Disclosure: The opinions expressed within this blog post are as of the date of publication and are provided for informational purposes only. Content will not be updated after publication and should not be considered current after the publication date. All opinions are subject to change without notice, and due to changes in the market or economic conditions may not necessarily come to pass. Nothing contained herein should be construed as a comprehensive statement of the matters discussed, considered investment, financial, legal, or tax advice, or a recommendation to buy or sell any securities, and no investment decision should be made based solely on any information provided herein. Links to third party content are included for convenience only, we do not endorse, sponsor, or recommend any of the third parties or their websites and do not guarantee the adequacy of information contained within their websites.