Our client portfolios have benefited from diversification as a wide range of asset classes had positive returns for the quarter and many of the funds we hold performed fairly well. Notably, international stocks led large U.S. stocks, even with currency movements eating into foreign returns for U.S. dollar-based investors. Smaller U.S. companies outperformed large companies for the first time in a great while. The bond market was also positive as Treasury yields declined over the quarter. Our tactical positions in flexible bond funds generally outpaced core bonds over the quarter and continued to add value.

Despite some recent data that have been a little soft, the U.S. economy appears to be in fairly good shape overall. The employment picture has vastly improved since the recession, and economic growth has been modestly positive; enough that the Federal Reserve (“Fed”) has hinted it may begin interest rate hikes later this year. However, the strong dollar has hurt export growth, and U.S. consumer spending hasn’t shown material improvement amidst persistently sluggish wage growth. The decline in oil prices continues to keep a lid on inflation. It has also caused cutbacks in production, which in turn has begun to take a bite out of employment growth and industrial production. It’s too early to tell if these are new long-term trends or short-term adjustments.

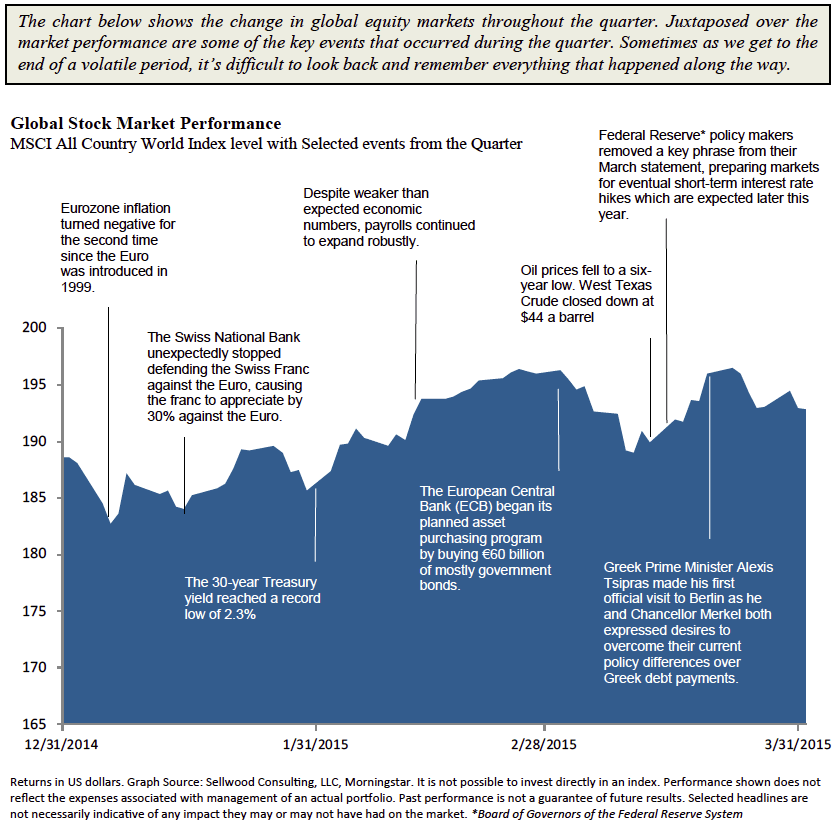

At the other end of the policy spectrum, the European Central Bank (ECB) finally launched quantitative easing (bond buying) during the quarter in an effort to boost Europe’s stalled economy. With the Bank of Japan and the People’s Bank of China also undertaking stimulus efforts, there is no shortage of central bank support for global financial markets.

Portfolio Commentary

Durability and resilience are characteristics we take very seriously when it comes to portfolio construction. At the simplest level, this means building diversified portfolios that have multiple paths to positive returns and protection against multiple risks. Over time, this approach should enable us to generate strong returns at appropriate risk levels, as has been the case over our history.

When investing the stock portion of our portfolio strategies, we are mindful of risk factors, primarily that U.S. stocks are expensive. It is also the case that Fed support, which has been critical to the post-financial-crisis stock market rally, is slowly being scaled back. Looking forward, in our view the most likely scenario is fairly low U.S. equity returns over the next five years. But despite this outlook, we recognize that stocks remain attractive relative to a lot of other asset classes and so could continue to perform well for some time. As a result we continue to own a meaningful allocation to U.S. stocks in the portfolios but hold a lower weight than we would if return potential were higher.

European stocks have not enjoyed the same level of gains as U.S. stocks in recent years, making them more attractively priced today with stronger return potential. That European stocks have lagged hasn’t necessarily been surprising given the poor economic health of the region and the ongoing questions about the durability of the Eurozone itself. But the thing about investing is that at lower prices the picture doesn’t have to be rosy because investors are getting the asset class more cheaply with presumably more upside potential. (This isn’t automatically the case, and this is why careful analysis of the opportunity is the critical factor for success.)

In this instance, we believe European stocks are priced to generate attractive returns if we look out five years and assume a return to more normal economic and earnings growth. This is precisely what the ECB is attempting to engineer. As a result, our portfolios own a nearly full strategic weighting in developed international stocks, though we have not added tactically to this position. We’d prefer to see even stronger upside potential before doing so.

Emerging markets have been buffeted by a variety of investor worries. A significant concern is China’s slowing growth rate and the potential for a sharper downturn as the government seeks to get the economy on a more sustainable path. As China’s growth rate has come down over the past few years, some of that risk has been priced in, and we are at present reassessing the remaining downside. We think it is prudent to factor in a healthy margin of safety (i.e., a higher return requirement for us to add more exposure to this asset class) to account for this and other risks. Considering both the potential rewards and risks in emerging markets, we have maintained some exposure to this asset class.

In structuring our clients’ bond allocation, interest rates will be the predominant factor in determining future bond returns. Since we do not have the ability to predict when or if rates will rise, we consider a range of assumptions for where interest rates will be five years out as part of the scenario analysis framework that is at the heart of our portfolio decision-making.

Today, even our most pessimistic scenario yields the same conclusion about core bonds—returns over the next five years are likely to be very low, regardless of whether rates decline from 1.95% (where they ended the quarter) or rise. As a result, we own less in core bond funds and have instead invested in a number of more flexible fixed-income strategies with broad mandates. This should achieve better performance through a variety of interest-rate climates. That said, even with their low return potential, core bonds remain a key tool in protecting against stock market losses, and so we maintain an allocation in our portfolios.

We know that not all risks we manage against will play out, and in many cases there will be a small price to pay for that insurance. We also know it can take time for our investment thesis to be rewarded (which is why our decisions are not based on a short-term view), and there may be periods when few opportunities are compelling. These are some of the challenges of the past few years. We are confident that over time our integration of risk and return considerations should result in sound, well-performing portfolios that help our clients meet their financial goals.

As always, we appreciate your confidence and welcome questions about your individual situation.

Download this First Quarter 2015 Investment Review report as a PDF (110kb). Visit our archives for reports on past quarters.