As financial planners, we run a lot of retirement projections. We tend to assume a long life to account for the financial impact of longevity. Long life in our projections is typically age 96. The idea is that there is a relatively low chance of living past age 95, so age 96 forms the outer edge of a long life.

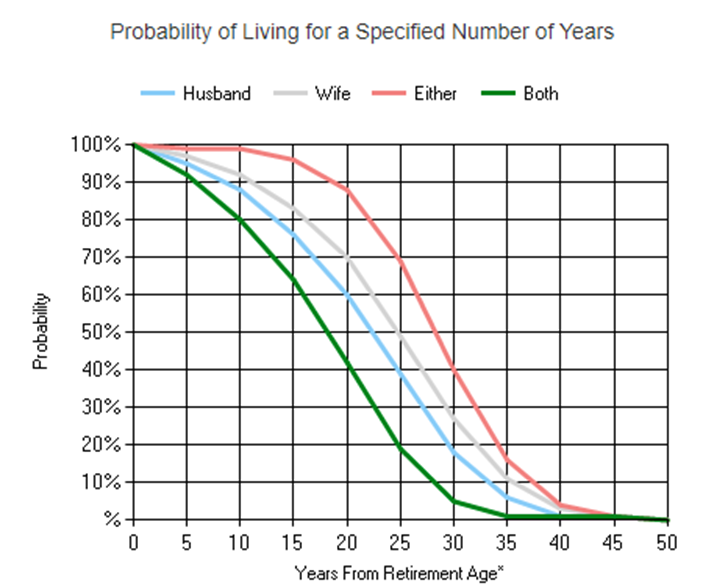

In actuality, the chances of reaching age 95 are high if you have reached age 65 and are in very good health. According to the Social Security Administration’s 2022 OASDI Trustees report, there is an over 30% chance of an age 65 woman in excellent health living until age 95. The chances of one of a married age 65 couple living to age 95 is even higher at 40%!

Chances of Living to 100

What about your chances of living to be 100? According to the 2022 OASDI Trustees report, the chances of a non-smoking age 65 woman in excellent health living until age 100 is 13%, and the chances of one of a married age 65 couple living to age 100 19%. There are about 90,000 “Centenarians” in the U.S. today, which is less than 1% of the population.

However, that is not the whole story. It turns out that Centenarians have a thing or two to teach us about reaching that advanced age ourselves. Studies of people who have reached age 100 have revealed common characteristics of Centenarians.

FAQS

We’re happy to answer any questions you have about our firm and our processes. Here are answers to some of the questions we receive most frequently.

Lessons from the Blue Zones

Researchers have discovered that Centenarians are clustered in five different regions around the globe. These five regions have been coined, “Blue Zones.” The regions that make up the Blue Zones include Okinawa, Japan; Sardinia, Italy; Nicoya, Costa Rica; Icaria, Greece; and Loma Linda, California.

What’s so special about the “Blue Zones?” After all, these areas are quite different geographically. As it turns out, it’s the lifestyle people lead in those areas that makes the difference. People in these areas share nine key lifestyle habits, which have been coined the “Power 9” by Dan Buettner, an award-winning journalist, producer, and New York Times bestselling author.

The lifestyle habits Dan Buettner identified can be summed up as:

- Physical activity – Residents in the Blue Zones exercise throughout the day through activities like gardening, walking, and cooking.

- Purpose and positive outlook- Research on psychological well-being has linked a sense of purpose with a reduced risk of death. HThe evidence is clear; having a positive outlook on life can influence how long you live.

- Healthy eating- Blue Zone residents practice healthy eating. Limiting calories, limiting alcohol, and eating a plant-based diet are all commonalities.

- Manage stress – Blue Zone residents have routines that help manage their stress.

- Family, community, and social Life – People in Blue Zones have supportive social circles and actively participate in them. Family is a part of daily life, and family members support each other. Many of the Blue Zone residents are religious and find camaraderie and meaning in their faith-based community.

GUIDES

The Essential Guide to Retirement Planning

A 4-part series that answers key questions about building your plan, positioning your investments, and more.

Living Wisely- a different way to look at retirement

For those who plan to live many years after retiring, it’s wise to focus on emulating the lifestyle habits that have led residents in the Blue Zones to live to 100. This means making many small lifestyle choices that promote healthy eating, stress reduction, social engagement, and a positive outlook.

At our recent Living Wisely event, Healthy Living into Your 80s and 90s, we heard presentations from three prominent doctors who have dedicated their practices to helping people live long, healthy lives. Click here to see videos and download slides from the presentations.

Financial Planning for a “Centenarian” lifespan

Of course, the exception of living to be 100 means planning ahead to make your life savings last all those years as well. Decisions about income, investments, retirement plans, pensions, and social security benefits should all be part of your financial plan. Your investment plan should encompass this longer time horizon too, by including enough long-term growth investments to keep pace with inflation over many years. At Blankinship & Foster, our wealth management planning helps you make the most important decisions about finances, investments, tax planning and benefits planning as well as things like estate planning and insurance planning. Contact us to learn more about how we can help you plan for a long, healthy, and prosperous retirement.

Disclosure: The opinions expressed within this blog post are as of the date of publication and are provided for informational purposes only. Content will not be updated after publication and should not be considered current after the publication date. All opinions are subject to change without notice, and due to changes in the market or economic conditions may not necessarily come to pass. Nothing contained herein should be construed as a comprehensive statement of the matters discussed, considered investment, financial, legal, or tax advice, or a recommendation to buy or sell any securities, and no investment decision should be made based solely on any information provided herein. Links to third party content are included for convenience only, we do not endorse, sponsor, or recommend any of the third parties or their websites and do not guarantee the adequacy of information contained within their websites.