Donor-advised funds are the fastest-growing charitable giving vehicle in the United States. This is because they are one of the easiest and most tax-advantageous ways to give to charity. A Donor Advised Fund (DAF) basically functions like a charitable foundation but is much easier and less expensive to maintain. A change in the tax code in 2017 made Donor Advised Funds even more attractive to many Americans.

The reason this vehicle became more attractive after the 2017 tax changes is that a limit was imposed on itemized deductions – limits on state and local taxes, to be exact. At the same time, the 2017 changes drastically increased the standard deduction. This reduced the tax benefits of giving directly to charities because many people who used to be able to itemize charitable contributions of a few hundred or a few thousand dollars a year were no longer able to receive more deductions than the standard deduction. Most people continue to support their favorite charities, but they aren’t receiving the same tax benefits from doing so.

FAQS

We’re happy to answer any questions you have about our firm and our processes. Here are answers to some of the questions we receive most frequently.

The “deduction bunching” strategy

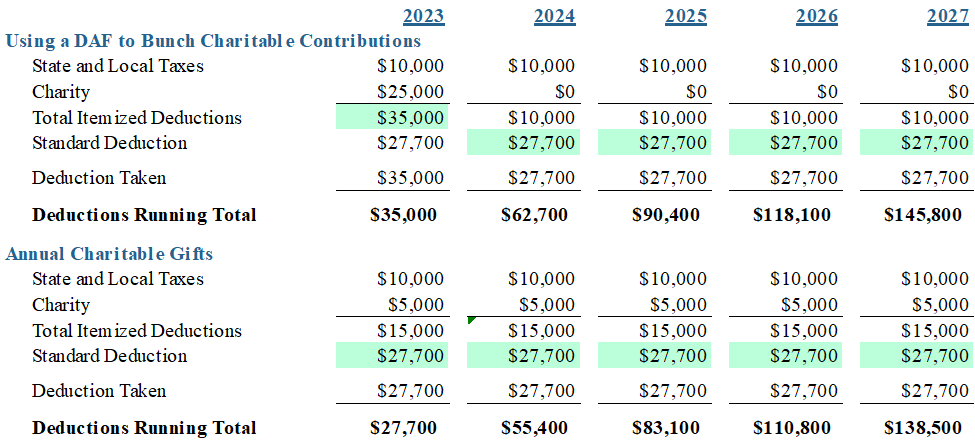

One strategy that was developed to get around this limitation was to combine several years’ worth of gifts into a single year. For example, instead of giving $5,000 to charity each year, you would give $25,000 in a single year then forgo the annual contributions. One of the simplest ways to do this is with a donor advised fund.

The strategy works like this. Suppose you would normally give $5,000 to charity, but that wasn’t enough to allow you to itemize your tax deductions. By funding a donor advised fund (DAF) with a large lump sum in one single tax year, you get the large itemized tax deduction in one year, then take the standard deduction for the next few years. At the end of five years, you would likely end up paying less in taxes than if you made non-deductible contributions to those same charities over 5 years.

As you can see in this example, your total deductions at the end of five years would be higher than if you just gave funds to the charity each year.

Know the rules

Donor Advised Funds are fairly easy to set up, but they do have some rules you need to be aware of.

- A donor advised fund can be used to pay for things like a paddle raise at a charitable gala, but it cannot be used for legally binding financial commitments like pledges you’ve made to a charity.

- A donor advised fund can be used to buy tickets to an event that you don’t plan to attend, or other support that is 100% tax deductible, but it could not be used to pay for sponsorships, dinner, or auction items at the event. That’s because these items have some benefit to you that is not tax deductible.

- Memberships that provide only incidental benefits can be funded by a donor advised fund. Because you often receive items in return for things like Zoo or public media memberships, you probably can’t use a DAF for these memberships, but you can the DAF to fund general gifts to these charities.

- A donor advised fund can be used to fund scholarships, so long as the donor or a related party isn’t a beneficiary of the scholarship, or the main person deciding who receives the scholarship.

ACCREDITATIONS & AWARDS

We’re proud to have been honored by some of the organizations in our industry.

Different types of DAFs

DAFs may be sponsored by a single charity, by a community foundation which serves many charities, or by a commercial organization such as Charles Schwab & Company. For commercial DAF’s, gifts can be directed as small as $100. And nearly any asset can be used to fund a DAF, including appreciated securities, real estate or even business interests. The sponsoring organization sells the asset, so you get an additional tax benefit by avoiding paying capital gains taxes.

In our practice, we’ve used Donor Advised Funds sponsored by Charles Schwab, the San Diego Foundation and Jewish Community Foundation, depending on the client’s needs and objectives and the complexity of the gift you want to use to fund the DAF. It really does give you more flexibility in your charitable and tax planning.

Disclosure: The opinions expressed within this blog post are as of the date of publication and are provided for informational purposes only. Content will not be updated after publication and should not be considered current after the publication date. All opinions are subject to change without notice, and due to changes in the market or economic conditions may not necessarily come to pass. Nothing contained herein should be construed as a comprehensive statement of the matters discussed, considered investment, financial, legal, or tax advice, or a recommendation to buy or sell any securities, and no investment decision should be made based solely on any information provided herein. Links to third party content are included for convenience only, we do not endorse, sponsor, or recommend any of the third parties or their websites and do not guarantee the adequacy of information contained within their websites.