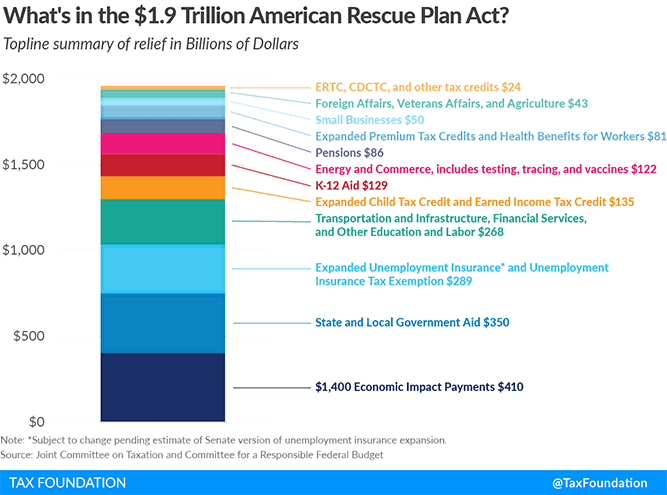

The third volley of stimulus has been fired in the U.S. government’s battle against COVID-19. Congress enacted the $2.2 Trillion CARES Act and the $2.3 Trillion Consolidated Appropriations Act in 2020. Now, Congress has enacted the $1.9 Trillion American Rescue Plan Act of 2021.

The American Rescue Plan Act (ARPA) distributes aid in all directions: state and local governments, hospitals and health systems, schools, businesses, nonprofits, and individuals.

In this article, we will focus on the provisions that affect individuals.

More stimulus payments

The American Rescue Plan Act (ARPA) will send a third stimulus payment of $1,400 for each taxpayer ($2,800 for joint filers), in addition to $1,400 per dependent. The full $1,400 is paid if the Adjusted Gross Income (AGI) is under $75,000 ($150,000 for joint filers). The payment is reduced for incomes above those amounts, and fully phased out for single filers with incomes above $75,000 ($150,000 for married filing jointly). Payments will be sent as direct deposits for those who e-filed their 2019 tax returns, and as checks in the mail for those who filed paper tax returns.

Child tax credit enhancements

ARPA makes the Child Tax Credit fully refundable for 2021 and increases the amount to $3,000 per child ($3,600 for a child under age 6). It increases the age of qualifying children by one year for 2021, such that 17-year-olds qualify for the credit. The enhanced credit begins to phase out for Adjusted Gross Income more than $150,000 for joint filers ($112,500 for head of household filers and $75,000 for other filers). It also makes the Child and Dependent Care Tax Credit fully refundable and increases the maximum credit rate to 50%.

FAQS

We’re happy to answer any questions you have about our firm and our processes. Here are answers to some of the questions we receive most frequently.

Credits for Paid Sick and Family Leave

The legislation extends the paid sick time and paid family leave credits created by the Families First Coronavirus Response Act from March 31, 2021 through September 30, 2021. It increases the amount of wages for which an employer may claim the paid family credit in a year from $10,000 to $12,000 per employee and increases the number of days for which self-employed individuals can claim the credit from 50 to 60. It also expands eligible leave to include time taken to receive or recover from a COVID-19 vaccine.

Unemployment insurance

The three federal unemployment insurance expansions first created by the CARES Act are extended through September 6, 2021. The legislation increases the total number of weeks of benefits available to individuals who cannot return to work safely from 50 to 79, matching the expiration of the broader UI benefits.

Also included is a new provision to exempt $10,200 of unemployment benefits received in 2020 from income taxes. The exclusion is retroactive, applying to unemployment insurance benefits received last year, largely to reduce the issue of surprise tax bills. It only applies to individuals with incomes below $150,000.

ACCREDITATIONS & AWARDS

We’re proud to have been honored by some of the organizations in our industry.

Planning opportunities from ARPA

If you will receive a stimulus payment and you can afford to save any of it, you can still make an IRA or Roth IRA contribution (if you qualify) for 2020. Thanks to an extended deadline for such contributions, you will have until May 17th. Traditional IRA contributions or 401K deferrals can help reduce your tax return income, which can help you avoid the phaseouts if you are near that level of income.

ARPA will likely not be the last major piece of legislation in 2021. The Biden Administration has laid out priorities for infrastructure and for major tax legislation as well. As always, our analysis and advice will be based on each client’s overall financial plan, changes in their situation, as well as the changes in the laws. Contact us to learn more about how we can help you.

Disclosure: The opinions expressed within this blog post are as of the date of publication and are provided for informational purposes only. Content will not be updated after publication and should not be considered current after the publication date. All opinions are subject to change without notice, and due to changes in the market or economic conditions may not necessarily come to pass. Nothing contained herein should be construed as a comprehensive statement of the matters discussed, considered investment, financial, legal, or tax advice, or a recommendation to buy or sell any securities, and no investment decision should be made based solely on any information provided herein. Links to third party content are included for convenience only, we do not endorse, sponsor, or recommend any of the third parties or their websites and do not guarantee the adequacy of information contained within their websites.