Quarterly Investment Review

The economy grew by 2% in the first quarter and is expected to grow by about 2.3% in the second quarter, based on widely followed indicator from the Federal Reserve Bank of Atlanta. Even as most economists expect a slowdown in economic growth and a rise in unemployment, the widely anticipated recession of 2023 remains elusive.

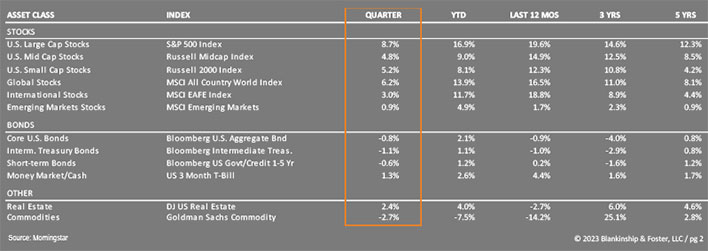

The stock market rally, which began in the fourth quarter of 2022 continued throughout the first half of 2023, buoyed by a resilient labor market and a pause in interest rate hikes by the U.S. Federal Reserve. The S&P 500 Index of large U.S. companies rose 8.7% in the second quarter and is up 16.9% year-to- date. The rally has been powered primarily by large (mostly technology) companies, with smaller companies (represented by the Russell 2000 Index) rising only 5.2% in the quarter and 8.1% so far this year. The MSCI EAFE index of international stocks rose 3.0% in the quarter and is up 11.7% this year. The bond market has been volatile, swinging between optimism that interest rate hikes were over and acceptance that more are coming. The benchmark 10-year Treasury yield ended the second quarter at 3.81%, roughly where it began the year but up for the quarter. As a result, bonds lost 0.8% during the second quarter but have still gained 2.1% for the year as higher yields helped to offset falling prices (bond prices fall when market interest rates rise). High Yield “Junk” bonds rose 1.8% during the quarter, representing optimism about corporate finances, at least in the short-term. The Dow Jones U.S. Real Estate Index rose 2.4% during the quarter.

Economy

Once again, the economy is not currently in a recession, though the probability that one is coming has risen in recent weeks. Looking at the treasury yield curve, where short-term interest rates are significantly higher than longer-term rates (the yield curve is inverted), this suggests a fairly high probability of a recession in the near-term. An inversion of the yield curve does not guarantee that a recession is coming, but it has preceded every recession since 1950.

More importantly, looking under the hood at different segments of the economy, several factors suggest that business and consumer spending are likely to slow in the coming months. From layoffs in key economic sectors like technology to weakness in commercial real estate markets and low personal savings rates, the economy looks to be slowing from its current pace of 2% growth. That doesn’t mean a recession is imminent, but it does mean that there is less room to absorb shocks if (or more likely when) they come.

The Fed’s campaign to target inflation by raising interest rates seems to have been successful. Inflation has fallen from its high last summer of 9.1% to just 3.0% (year-over-year) in June. Looking at the components of inflation, most have cooled considerably. Even housing costs are starting to ease a bit. We expect to see inflation moderating to around 3.5% by year-end and perhaps 2-3% by the end of 2024, which would allow the Federal Reserve to begin lowering interest rates. This is what the market seems to be expecting given that long-term Treasury interest rates are lower than short-term rates.

The wild card remains the labor force, which has shrunk over the past few years. Skill gaps (the difference between what employers need and what they can find in the marketplace) remain stubbornly high, keeping upward pressure on wages while also putting a lid on how high unemployment can rise. Employment is a lagging indicator of economic health, so we have to be careful placing too much hope in low unemployment (which is always lowest right before a recession begins), but the strength of the labor market does give some forecasters the confidence to suggest that any impending recession might be relatively mild or short-lived (or both).

Growth is looking a bit firmer around the world than it did even earlier this year. While manufacturing has hit a bit of a soft patch, most countries continue to show some level of expansion. Lower energy prices in Europe and a post-COVID recovery in China are reasons for some optimism.

Outlook

Many factors have contributed to a slowing economy, and it’s not a foregone conclusion that a recession must occur. As we noted last quarter and above, it does seem more likely, though the consensus seems to point to a recession beginning in 2024 rather than later this year. The stock market resilience is largely a reflection of a combination of better-than-expected earnings and a recovery from lower valuations reached after last year’s selloff. It remains to be seen whether that optimism will be rewarded with continued gains in stock prices or renewed selling on economic weakness. What does seem likely is increased volatility in the coming months as investors try to reassess the odds of growth and weakness. Major shocks like a government shutdown or a significant strike (UPS) cannot be ruled out, either.

FAQS

We’re happy to answer any questions you have about our firm and our processes. Here are answers to some of the questions we receive most frequently.

Looking forward, current valuations of stocks and bonds remain somewhat attractive even after the quarter’s strong performance. Five-year expected returns on investments have improved significantly since the market peak in 2022. Even though stocks have risen recently, bond markets have priced in a fairly significant reduction in interest rates, signaling an expectation of a recession in the coming quarters. We would not be surprised by a drop in stock prices on economic weakness, followed by a strong recovery by the end of 2024, though other scenarios are also possible.

One thing that is a bit disconcerting is just how narrow the stock market has become, meaning that the gains we’re seeing in the indexes are really powered by just a handful of big (mostly tech) companies. This behavior is typically observed late in a bull market.

More to the point, it’s nearly impossible to time stock market movements like we’ve described above. Historically, periods when consumer sentiment about the economy were at its worst were some of the best times to buy stocks. Equity prices are likely to be volatile this year as investors weigh the impact of a looming (or avoided) recession and negotiations in Washington around funding the government for 2024.

Our Portfolios

Our stock exposure is currently broad based and weighted towards large U.S. companies. Our value bias, which helped last year as high-flying growth companies struggled with rising interest rates, has been a bit of a detractor this year as investors have shrugged off high interest rates and paid up for the stocks of companies that are showing earnings growth. If a recession does occur, we would expect this trend to reverse again and those higher P/E (expensive) stocks should fall harder than the rest of the market. Our international exposure remains balanced between hedged and unhedged investments and benefits from more attractive valuations than comparable U.S. equities.

ARTICLE

Invest $100K the Right Way

At some point, you may find yourself with $100,000 in the bank and questions on how to invest it.

Today’s higher interest rates mean that expected bond returns going forward are more attractive than they were a year ago. More importantly, if our expectation of a recession is realized, interest rates will likely settle back down, providing good returns to bonds should stocks falter heading into a recession. Bonds should be a better diversifier this year, especially if markets are correct in forecasting lower interest rates heading into 2024. Even if that expectation is unrealized, longer-term interest rates have risen quite a bit already and are unlikely to rise significantly. And as we’ve pointed out, the higher current yields help to offset the consequences of further increases in long-term interest rates.

In short, we continue to expect volatility as investors prepare for a possible recession and adjust their estimates for stock prices accordingly. We’ll use such periods of volatility to rebalance portfolios and pick up stocks (or bonds) at discounted prices, to better profit from the recovery that has followed every single market decline for as long as there have been markets.

As always, we are here for you and are ready to provide the guidance and planning you expect from us. If you have any questions about your investments or your financial plan, we would love the opportunity to discuss them with you.

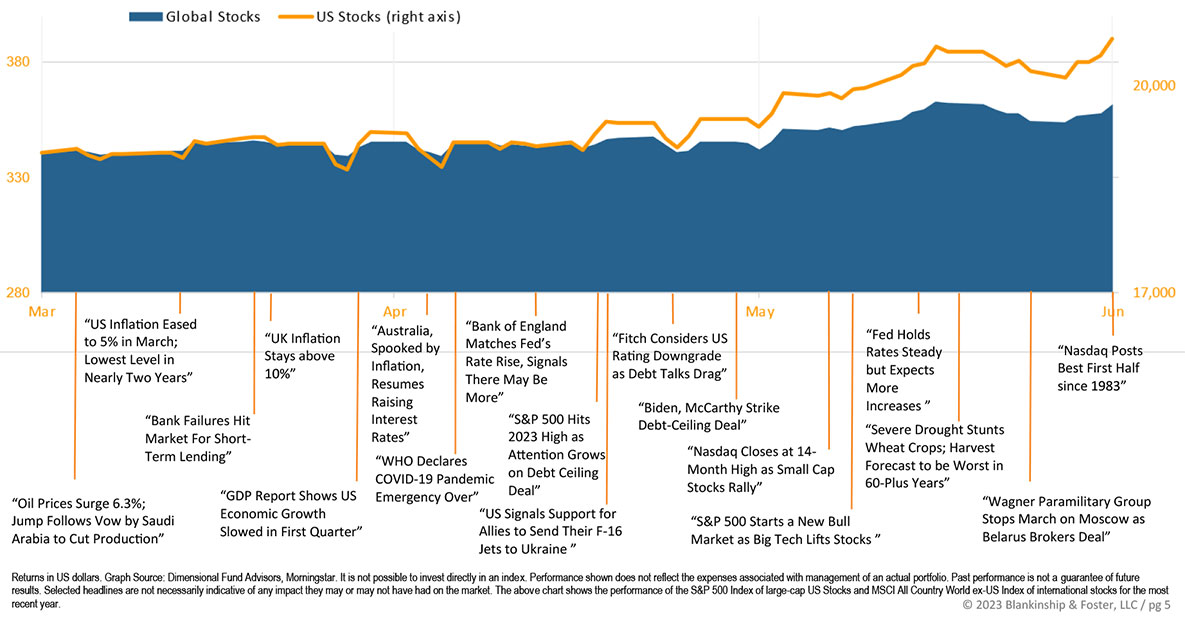

Global Stock Market Performance

The chart below shows the change in global equity markets throughout the quarter. Juxtaposed over the market performance are some of the key events that occurred during the period. Sometimes as we get to the end of a volatile period, it’s difficult to look back and remember everything that happened along the way.

Past performance is not an indication of future returns. Information and opinions provided herein reflect the views of the author as of the publication date of this article. Such views and opinions are subject to change at any point and without notice. Some of the information provided herein was obtained from third-party sources believed to be reliable but such information is not guaranteed to be accurate.

The content is being provided for informational purposes only, and nothing within is, or is intended to constitute, investment, tax, or legal advice or a recommendation to buy or sell any types of securities or investments. The author has not considered the investment objectives, financial situation, or particular needs of any individual investor. Any forward-looking statements or forecasts are based on assumptions only, and actual results are expected to vary from any such statements or forecasts. No reliance should be placed on any such statements or forecasts when making any investment decision. Any assumptions and projections displayed are estimates, hypothetical in nature, and meant to serve solely as a guideline. No investment decision should be made based solely on any information provided herein.

There is a risk of loss from an investment in securities, including the risk of total loss of principal, which an investor will need to be prepared to bear. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment will be profitable or suitable for a particular investor’s financial situation or risk tolerance.

Blankinship & Foster is an investment adviser registered with the Securities & Exchange Commission (SEC). However, such registration does not imply a certain level of skill or training and no inference to the contrary should be made. Complete information about our services and fees is contained in our Form ADV Part 2A (Disclosure Brochure), a copy of which can be obtained at www.adviserinfo.sec.gov or by calling us at (858) 755-5166, or by visiting our website at www.bfadvisors.com.