Quarter In Review

Despite its reputation as the worst seasonal period for stocks, the U.S. market delivered strong returns in the third quarter (up 4.5%), extending its winning streak to eight consecutive quarters and a remarkable 18 out of the last 19 quarters. But the lead story was once again the strength of foreign markets. For the third consecutive quarter, the U.S. dollar declined against major foreign currencies, boosting returns for dollar-based investors. Emerging markets surged almost 8% and European stocks gained 6.6%.

In the U.S., large company growth stocks—technology stocks in particular—outperformed the broad market, up more than 20% this year, compared to the S&P 500 index which is up 14.2%. Smaller company stocks have returned 11%. Energy stocks had a big rebound in September (up 10%) as oil prices rose above fifty dollars. But for the year, the sector is still down 6.6%, while technology and health care have soared 24% and 20%, respectively.

In the fixed-income markets, core investment-grade bonds inched up 0.9% for the quarter. Core bond prices peaked in early September as the 10-year Treasury yield (which moves inversely to bond prices) bottomed at 2.05% amid tensions with North Korea, catastrophic hurricanes in Texas and Florida, and a potential U.S. debt ceiling crisis/government shutdown. But the yield shot up into month-end, closing the quarter at 2.33%—right about where it stood three months earlier and erasing bond price gains in the early part of the quarter. Credit-sensitive sectors of the fixed-income market outperformed core bonds for the quarter, with the high-yield bond index gaining 2%.

Our Portfolios

For the quarter, our globally diversified portfolios generated attractive returns as all the major asset classes registered gains for the period. Consistent with what we’ve seen this year, our portfolios benefited from our exposure to emerging-market and international stocks, both of which are seeing improvements in corporate earnings (and stock market) performance. And yet, foreign earnings remain far below their pre-crisis highs and also below what we view as their (longer-term) trend growth level. We therefore see plenty of potential for additional outperformance over the long-term.

At approximately 25 times last year’s earnings, we still think that the U.S. stock market remains generally overvalued, limiting upside potential over the next few years. We expect somewhat better results from our international and emerging markets positions over this time frame.

Our fixed-income positions contributed modestly within the quarter, as our long-established positions in flexible and absolute-return-oriented bond funds outpaced core investment-grade bonds during the quarter and the year-to-date. High yield bond funds also bested the core bond index over the quarter and continue to provide a valuable hedge for our portfolios against rising interest rates as their yields are positively correlated to rate changes.

Our investments in diversifiers (both growth and income) have been generally positive. Our pipeline fund positions have struggled recently with a combination of volatile oil prices and hurricane related disruptions, derailing a recovery from the oil price crash of 2015. Also, our riskier high yield municipal bond positions have been impacted by the default in Puerto Rico followed by the devastation of Hurricanes Irma and Maria and a late quarter rise in interest rates. Our diversifying positions cumulatively outperformed core bonds but lagged the strong U.S. stock market.

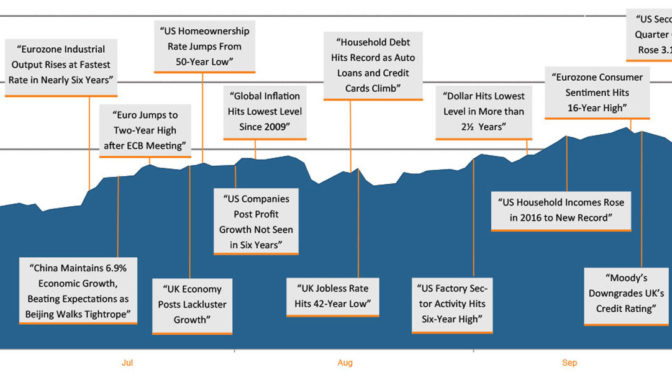

Global Stock Market Performance The chart shows the change in global equity markets throughout the quarter. Juxtaposed over the market performance are some of the key events that occurred during the period. Sometimes as we get to the end of a volatile period, it’s difficult to look back and remember everything that happened along the way.

Returns in US dollars. Graph Source: Dimensional Fund Advisors, Morningstar. It is not possible to invest directly in an index. Performance shown does not reflect the expenses associated with management of an actual portfolio. Past performance is not a guarantee of future results. Selected headlines are not necessarily indicative of any impact they may or may not have had on the market.

Economic Environment

We are optimistic as we look ahead to the remainder of the year. The synchronized global economic growth recovery continues apace, providing a solid foundation for corporate earnings and financial assets in general.

Real (net-of-inflation) policy interest rates remain in negative territory across all the major developed economies, and the European Central Bank and Bank of Japan continue purchasing assets via quantitative easing. Meanwhile, easing inflationary pressures in emerging markets have allowed numerous emerging-market central banks to lower interest rates this year (including Brazil, Russia, India, and South Africa). Lower inflation and lower central bank policy rates are typically positive for local stock markets, and they can also help offset the impact of policy tightening by the Fed on these markets.

Domestically, while real GDP growth remains subpar by historical standards, it continues to grind along at around a 2% annual rate. This is consistent with research about the long-term impact of financial crises on economies. Despite the Federal Reserve raising short-term interest rates (“tightening financial policy”), financial conditions have actually eased over the past year due to factors such as the declining dollar, higher stock prices, narrower corporate bond spreads, and lower Treasury bond yields. Each of these help U.S. companies sell goods or invest in their businesses, and should be supportive for economic activity, at least over the short term.

Although the Macro backdrop is attractive, we remain cognizant of the known and unknown risk factors. Historically high domestic equity valuations, fiscal policy changes that have yet to be enacted (e.g., tax reform, Obamacare repeal), and future tightening by the Fed are all known risks. North Korea is a risk we cannot handicap, but if the subdued market volatility of the past year is any indicator, investors have judged the risk of armed conflict as negligible (for now). Absent the outbreak of full scale war, any headline news seems likely to have a short-term market impact rather than a longer-term one.

Finally, as the Federal Reserve continues to move towards higher interest rates, the likelihood of a recession increases. With that in mind, we believe our client portfolios are tilted to the assets that have more attractive long-term risk/return profiles while remaining resilient across a range of scenarios. Our portfolios are diversified across investment strategies, asset classes, and risk exposures in an attempt to reduce risk. Still, risk is part of investing, and we must accept some well considered downside risk in order to capture current market gains.

As stable as markets have been recently, we know this won’t continue forever. It is impossible to completely avoid shorter-term volatility or downside risk. We therefore remain cognizant of, and prepared for, the periods of higher volatility that are certain to come within our long-term investing horizon. This includes regularly revisiting our analysis and keeping our focus on managing downside risks as we seek to capture positive long-term returns for our portfolios.

As always, we appreciate your confidence and welcome questions.

Download this Third Quarter 2017 Investment Review as a PDF (1.2 MB).

View reports on past quarters here.