Global markets were relatively calm for most of the quarter until June, when unexpected news from Europe shocked investors around the globe. Upending most forecasts and taking world financial markets by surprise, the United Kingdom voted to leave the European Union on June 23 (“Brexit”). In the wake of the vote, British pound sterling fell 11% overnight against the U.S. dollar—its lowest level since 1985. The euro fell 2.4% to 1.10 versus the dollar. Global equities dropped sharply.

In the week following Britain’s historic vote, despite significant uncertainty regarding the economic, political, and financial market implications of Brexit, global equities rallied. When the dust had settled, international stocks remained in the red, while U.S. stocks made a full recovery, gaining 2.5% for the quarter. Emerging markets returned a positive 0.7% for the quarter as the Chinese economy stabilized and many countries began to benefit from rising energy prices.

Before the Brexit vote, the big story in financial markets had been bonds, specifically negative yields on government bonds across the globe. By month’s end, the amount of government debt sporting negative yields had soared by nearly $1 trillion. Falling yields had been driven by economic growth concerns, central banks’ interest rate policy changes, and increased demand for safe assets.

The drop in interest rates across the globe has caused U.S. bond markets to rally, returning 2.2% for the quarter and 5.3% year to date. While we do not expect a sharp rise in interest rates any time soon, expected returns for core bonds are extremely low. Investors holding U.S. government bonds are earning very little, not enough to keep up with inflation in most cases. Worse still, those holding Japanese and German government bonds won’t even get all their money back when the bonds mature since those bonds are paying negative yields.

Conversely, yields remain attractive for flexible fixed-income strategies where managers can invest across a wide range of bonds, including high-yield corporate, mortgage and international government and corporate bonds. We saw strong performance for flexible fixed-income strategies, with most of them beating the core bond index for the quarter.

Portfolio Review and Positioning

Our current analysis continues to suggest that U.S. stocks are trading somewhat above their fair value. Therefore, we are still slightly underweight U.S. stocks. The expected returns for core bonds are quite unattractive, so we are also underweight to them. Instead, we are invested in what we believe is a more attractive mix of asset classes and strategies that our analysis suggests have more return potential. These assets, along with our exposure to U.S. stocks and core bonds, can be combined in a well-diversified, risk-managed portfolio.

We continue to favor developed international and emerging-markets equities. Our analysis suggests both these broad markets offer attractive five-year return potential, driven by improving earnings growth and expanding valuation multiples. Given additional uncertainty brought about by the Brexit, there is higher potential downside risk and volatility from these markets. However, unlike our expectations for U.S. stocks, we believe you should be rewarded for taking on these near-term risks.

Part of our underweight to U.S. stocks in our portfolios is also allocated to other asset classes, including energy infrastructure Master Limited Partnerships (“MLPs”), real estate and emerging markets debt. With these investments, we generally expect to get returns comparable to U.S. stocks over the long run. However, they behave differently than U.S. equities since they are influenced by factors beyond our economy. MLPs returns, for example, were impacted by commodity prices over the last year. However, over the long run, it is shaped by the volume of oil and natural gas being transported in pipelines and by changes in long term interest rates. Owning such diversifiers improves the overall potential risk-adjusted return of the portfolios.

Turning to the fixed-income side, we are underweight core bonds in favor of actively managed, flexible, unconstrained, and/or opportunistic fixed income funds. We expect to earn a meaningful return premium from these funds relative to the core bond index over the next several years. In exchange for the higher expected returns, we know we are taking on more credit risk. These bonds may not hold up as well if there is deflation, a short-term flight-to-safety event, or shock that pushes Treasury bond yields even lower. However, these flexible fixed-income funds have less sensitivity to negative price impacts from rising Treasury rates. Therefore, in addition to positive expected excess returns, they play a valuable risk-management role in your portfolios.

Looking Ahead

While the initial market reaction to Brexit is behind us, its long term economic impact is difficult to assess. This vote could increase the odds of a global recession. It also raises the risk that other countries could contemplate similar moves. It is uncertain how this will play out and what the effects will be. We do know that these factors may increase the likelihood and magnitude of shorter-term downside risk. It is our responsibility to safeguard the assets clients place with us by adhering to our investment discipline of riding out short-term swings and only adding tactical exposure when our view of valuations and expected returns is warranted.

Remaining focused on the long-term objective is key. Successful investing requires patience and the understanding that investing is a part of a process, not a one-off decision, toward achieving your long-term financial goals. Inevitably, there will be unpredictable shorter-term market ups and downs along the way. This kind of market volatility can certainly make for sleepless nights. We believe that overreacting to these market shocks is the wrong response for investors with a long-term investment focus.

As always, we appreciate your confidence and welcome any questions you might have.

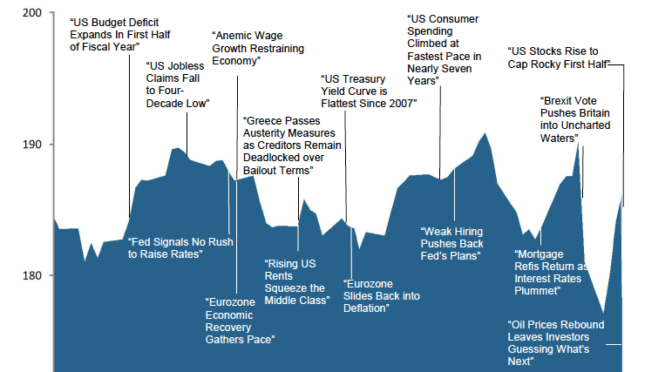

This chart shows the change in global equity markets throughout the quarter. Juxtaposed over the market performance are some of the key events that occurred during the quarter. Sometimes as we get to the end of a volatile period, it’s difficult to look back and remember everything that happened along the way.†

†Returns in US dollars. Graph Source: Dimensional Fund Advisors, Morningstar. It is not possible to invest directly in an index. Performance shown does not reflect the expenses associated with management of an actual portfolio. Past performance is not a guarantee of future results. Selected headlines are not necessarily indicative of any impact they may or may not have had on the market. *Board of Governors of the Federal Reserve System.

Global markets were relatively calm for most of the quarter until June, when unexpected news from Europe shocked investors around the globe. Upending most forecasts and taking world financial markets by surprise, the United Kingdom voted to leave the European Union on June 23 (“Brexit”). In the wake of the vote, British pound sterling fell 11% overnight against the U.S. dollar—its lowest level since 1985. The euro fell 2.4% to 1.10 versus the dollar. Global equities dropped sharply.

Global markets were relatively calm for most of the quarter until June, when unexpected news from Europe shocked investors around the globe. Upending most forecasts and taking world financial markets by surprise, the United Kingdom voted to leave the European Union on June 23 (“Brexit”). In the wake of the vote, British pound sterling fell 11% overnight against the U.S. dollar—its lowest level since 1985. The euro fell 2.4% to 1.10 versus the dollar. Global equities dropped sharply.