Quarter in Review

The volatile markets during the first quarter presented our portfolios with a real-world stress-test. Late December weakness became a rout in January, causing the worst start to a year in Wall Street history. Major equity markets dropped 10% to 16%, oil prices plunged, and fears of a global recession grew on the back of December’s soft economic reports.

Mid-February, everything changed, though there was no clear catalyst for the turnaround. Oil prices spiked higher, stock markets rallied and the dollar declined (improving unhedged foreign equity returns). In a welcome change for our portfolios, emerging-markets stocks were among the highest returning asset classes. Core bonds had rallied strongly in the first half of the quarter as interest rates fell but reversed during the second half as stock markets recovered and the 10-year Treasury yield moved higher.

This sort of extreme market turmoil vividly illustrates why we construct diversified investment portfolios for our clients. It also points out the unpredictability of short-term market movements. Our approach is to analyze long-term risk and return potential and build portfolios that both balance these considerations and are resilient across a variety of market scenarios.

During the first half of the quarter, our defensive positions in core bonds and diversifying strategies helped offset the dramatic equity market declines.

As the market rebounded, our flexible and absolute-return-oriented bond funds were rewarded. On the equity side, our allocations to emerging-markets and U.S. Large Cap stocks boosted performance as each asset class ended a rough quarter in positive territory (5.7% and 1.3%, respectively). Developed international stocks also rebounded dramatically off their mid-quarter lows but still finished the quarter down about 3%.

Portfolio Review and Positioning

We believe that part of successful investing involves riding out these nervous markets in which prices are driven by short-term news and investor cycles of emotion, staying focused on long-term fundamentals and remaining committed to a disciplined risk-management process. The quarter’s volatility seemed to reflect a growing recognition by investors of some of the macroeconomic concerns about which we have commented over the last few years. These include the uncertainty created by unprecedented monetary policies (which have resulted in ultra-low and even negative interest rates) and the potential effects of an economic slowdown in China on global markets. Our assessment of these risks has not materially changed, and we have factored them into our asset allocation decisions.

Economic growth, measured as growth in Gross Domestic Product (GDP) since 2009 has been sub-par at about 2% per year after inflation, compared to the post-war average of about 3.2%. At 82 months, the current expansion is longer than average. But absent an external shock, the U.S. economy seems to be in decent shape overall. Consumer balance sheets have improved, housing and job markets are in good shape, and low inflation suggests little risk of overheating in the economy. Despite investor concerns, we are confident that the U.S. is not entering a new recession.

That said, our analysis does suggest the U.S. stock market appears somewhat overvalued. Company earnings are an important factor in valuing stocks and until recently have set repeated records. But profits are also cyclical and can’t keep setting records forever. Company earnings have backed off from recent peak levels, suggesting that stock market returns over the next few years are likely to be modest, especially compared to the outsized gains we’ve seen since 2009. This assessment has been key in supporting the relatively conservative allocation to U.S. stocks in our portfolios.

Foreign stocks, by comparison, are almost a mirror image of the U.S. market. We see the potential for faster earnings growth from current below-normal levels. When we combine improving earnings with below average valuations, we see opportunities for much better returns from foreign stocks than U.S. stocks. To the valuation point, foreign stocks have seen very steep declines of 24%–35% from their April 2015 highs. This has essentially priced in a recession well before it’s clear there will be one.

Foreign stocks have discounted a lot of bad news and are set up for a potential rebound should investors realize things aren’t as bad as prices suggest. The rebound in Emerging Markets toward the end of the quarter is encouraging, suggesting our exposure to foreign stocks may be more helpful in future years than the recent past.

In the current ultra-low interest rate environment, allocating to fixed-income calls for greater ingenuity than in more normal conditions. While our core (high quality) bond positions can be a helpful stabilizer in difficult markets, their longer-term upside potential is very limited. Therefore, we look to our flexible and absolute-return-oriented bond funds to provide greater upside over the longer term, as they are better equipped to navigate a rising interest rate environment.

These holdings, which tend to focus on higher yielding corporate and foreign bonds, have been a key component in positioning our portfolios for rising interest rates. The trade-off is that these bonds aren’t as helpful when investors grow cautious, which we’ve seen during the past quarter. We still believe these positions are important as we position our portfolios for rising interest rates, even if it may add some volatility to our portfolios in the short-term.

Looking Ahead

Markets are cyclical, and for the past several years our portfolios have been facing some meaningful cyclical performance headwinds given our long-term, valuation-driven investment approach.

Our assessment of asset valuation is key to this approach, but asset valuations can take time to fully play out. In the interim, our portfolios are positioned for what we expect are the most likely outcomes: rising interest rates, modest U.S. stock market gains, and improving returns from foreign investments. Our portfolios are broadly diversified to capitalize on these themes while limiting the potential impact of an unexpected shock.

As always, we appreciate your confidence and welcome any questions you might have.

Download this First Quarter 2016 Investment Review as a PDF (125kb). View reports on past quarters here.

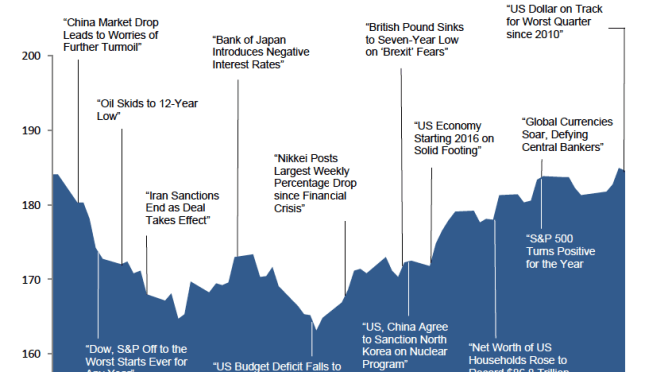

The chart below shows the change in global equity markets throughout the quarter. Juxtaposed over the market performance are some of the key events that occurred during the quarter. Sometimes as we get to the end of a volatile period, it’s difficult to look back and remember everything that happened along the way.

†Returns in US dollars. Graph Source: Dimensional Fund Advisors, Morningstar. It is not possible to invest directly in an index. Performance shown does not reflect the expenses associated with management of an actual portfolio. Past performance is not a guarantee of future results. Selected headlines are not necessarily indicative of any impact they may or may not have had on the market. *Board of Governors of the Federal Reserve System.