Quarter In Review

So far, 2017 has emerged to be a very positive one for global stock markets, and the second quarter was no exception. We saw developed international stocks jump 6.1% while emerging-market and larger-cap U.S. stocks gained 6.3% and 3.1%, respectively. Bonds continued their solid returns for the second consecutive quarter this year as market interest rates have gradually slid from post-election highs (bond prices rise when interest rates fall). Diversifying assets, like commodities and real estate were mixed, showing returns of -5.5% and 2.6%, respectively.

Economic Environment

Economic and corporate fundamentals largely still look sound, if uninspiring, and investors appear to be pricing in expectations for continued earnings growth. That said, there are some indications that the current expansion, now in its ninth year, is starting to run out of steam. Auto sales and housing starts may be near cyclical peaks. More broadly, inventories have built up while capital goods orders have slowed; both signs of slowing growth. Finally, expectations of tax cuts and economic stimulus from the Republicans’ across-the-board victories in Washington have yet to be realized. Without some form of stimulus, economic growth appears poised to be modest for the next couple of years; in the neighborhood of 2% or so.

Arguably, with unemployment at 4.4%, stronger growth could put more upward pressure on inflation. As it stands, inflation is largely expected to remain near the Federal Reserve’s 2% target. With U.S. inflation pressure muted and global deflation fears easing, investors generally expect global central banks to stop easing interest rates and possibly even begin tightening monetary policy gradually. This could put some upward pressure on U.S. interest rates, but the Federal Reserve (“Fed”) has signaled its intention to go slowly, so interest rates should be expected to rise gently over the coming months as the Fed continues to raise short-term rates.

In summary, U.S. growth appears steady, with some minor headwinds off-setting solid momentum. It’s worth remembering that financial crises in general are often followed by extended periods of sub-par growth. The 2008 Financial Crisis was one of the most significant in history, and subpar growth should be expected as the recovery continues. Low inflation, gently rising interest rates, and modest growth should continue to support the U.S. stock market for the time being, despite relatively high valuations.

Overseas, beneficial conditions like lower valuations and more economic room to grow continue to favor foreign stocks over the U.S. market. In Europe specifically, the European Central Bank recently increased its economic growth forecasts for the Eurozone for this year and next, while the International Monetary Fund (IMF) slightly reduced its expectations for U.S. growth.

Across the Eurozone, banks are largely well capitalized and ready to lend, unemployment has fallen to multiyear lows and modest inflation has replaced fears of deflation. And as the overall economy recovers, so should company finances. Corporate profits have been surprising to the upside. In response, analysts’ forecasts for corporate earnings growth have increased from the single digits to the double digits, and we are seeing more and more Wall Street strategists recommending an overweight to foreign stocks (a position we have held for a while in our portfolios).

Similarly, we are seeing improvements in expectations for emerging-markets stocks, which are still attractively valued and should benefit from the combination of improving global economics, mild inflation and more modest interest rate expectations.

Changes in investor sentiment (and the capital flows this creates) can feed on themselves in a virtuous circle. As more money flows into these asset classes, it can boost prices and returns, attracting yet more inflows and driving prices higher. While European stocks continue to trade at attractive valuations relative to U.S. stocks, we will be closely watching this market as more investors seek to take advantage of this opportunity. As a general rule, we do not put much faith in momentum for long-term growth, preferring to focus on valuations and business fundamentals. But we do recognize that momentum can be a powerful factor in stock market returns and can continue for much longer than analysts expect.

Portfolio Positioning

Ultimately, our asset class weightings, and specifically our willingness to take on equity risk, rest on our assessment of the risk and return potential for each asset class as well as the objectives and risk threshold of each portfolio. We manage our portfolios and work with our clients to help achieve their goals, and these considerations are at the forefront of our decision making process.

Within our portfolios, we look to bonds for protection, capital preservation, and/or a regular income stream to meet current and future spending needs.

As interest rates rise, assuming the global economy stays on its current growth trend, we expect returns for core, investment-grade bonds to remain low and possibly even negative. Despite low expected returns, these positions still serve a valuable role in our portfolio construction; core bonds will be one of the few assets gaining value in the event of a stock market sell off or global crisis.

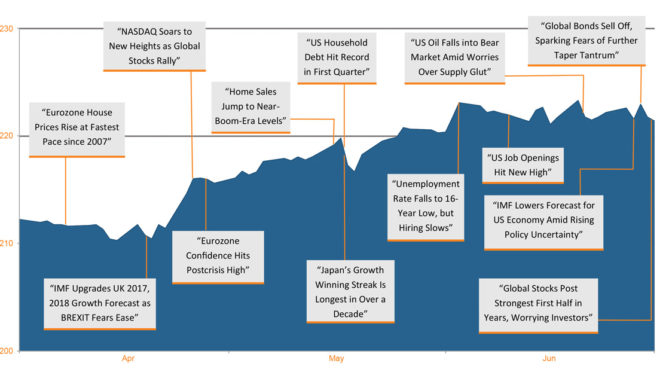

Global Stock Market Performance The chart below shows the change in global equity markets throughout the quarter. Juxtaposed over the market performance are some of the key events that occurred during the period. Sometimes as we get to the end of a volatile period, it’s difficult to look back and remember everything that happened along the way.

Returns in US dollars. Graph Source: Dimensional Fund Advisors, Morningstar. It is not possible to invest directly in an index. Performance shown does not reflect the expenses associated with management of an actual portfolio. Past performance is not a guarantee of future results. Selected headlines are not necessarily indicative of any impact they may or may not have had on the market.

Under current conditions, we anticipate returns for our more flexible bond funds to exceed those for core bonds, though they may also underperform in the event of a stock market correction. Overall, while the second quarter’s returns were mixed, our fixed income funds have generally done what we’ve needed (and expected) them to do in our portfolios so far this year. They’ve provided stability and modest income.

Which brings us to equities. Based on our analysis of valuations and longer-term earnings fundamentals—even putting aside any near-term political or geopolitical risks—U.S. stocks present very modest expected returns over the next five years. Valuation risk is high and offers no margin of safety in the event the optimistic scenario currently baked into market prices doesn’t play out. Therefore, we are underweight to U.S. stocks and to equity risk in general.

With minimal expectations for bonds and very modest expected returns on stocks, we continue to see long-term value from exposure to alternative strategies. While this has been a headwind to overall portfolio performance during extended periods of stock market gains, we continue to believe they are an important source of diversification, offering solid return potential and portfolio volatility reduction.

Given the low volatility in the markets so far this year, and exceptionally high stock market valuations, we think stocks may be particularly vulnerable in the event of a negative surprise. While we don’t see any particular near-term trigger for a sharp market decline, we know that short-term market surprises are part of investing. This is why it’s more important than ever to take a long-term investment view when it comes to positioning our portfolios. While there has seemed to be little need for diversified portfolios over the past eight years of a raging U.S. equity bull market, history teaches that this cycle will turn too and the portfolio benefits of strategies like alternatives and flexible fixed-income funds will then be apparent. Moreover, market over-reactions to shorter-term news can create compelling investment opportunities.

As always, we appreciate your confidence and welcome questions about your individual portfolio or financial situation.

Download this Second Quarter 2017 Investment Review as a PDF (1.2 MB).

View reports on past quarters here.